Economics (NCERT) Notes

Topics

All

Civil Services in India (26)

Ethics, Integrity and Aptitude

» Chapters from Book (11)

» Case Studies (8)

Solved Ethics Papers

» CSE - 2013 (18)

» CSE - 2014 (19)

» CSE - 2015 (17)

» CSE - 2016 (18)

» CSE - 2017 (19)

» CSE - 2018 (19)

» CSE - 2019 (19)

» CSE - 2020 (19)

» CSE - 2021 (19)

» CSE -2022 (17)

» CSE-2023 (17)

Essay and Answer Writing

» Quotes (34)

» Moral Stories (18)

» Anecdotes (11)

» Beautiful Poems (10)

» Chapters from Book (5)

» UPSC Essays (40)

» Model Essays (38)

» Research and Studies (4)

Economics (NCERT) Notes

» Class IX (14)

» Class X (16)

» Class XI (55)

» Class XII (53)

Economics Current (51)

International Affairs (20)

Polity and Governance (61)

Misc (77)

Select Topic »

Civil Services in India (26)

Ethics, Integrity and Aptitude (-)

» Chapters from Book (11)

» Case Studies (8)

Solved Ethics Papers (-)

» CSE - 2013 (18)

» CSE - 2014 (19)

» CSE - 2015 (17)

» CSE - 2016 (18)

» CSE - 2017 (19)

» CSE - 2018 (19)

» CSE - 2019 (19)

» CSE - 2020 (19)

» CSE - 2021 (19)

» CSE -2022 (17)

» CSE-2023 (17)

Essay and Answer Writing (-)

» Quotes (34)

» Moral Stories (18)

» Anecdotes (11)

» Beautiful Poems (10)

» Chapters from Book (5)

» UPSC Essays (40)

» Model Essays (38)

» Research and Studies (4)

Economics (NCERT) Notes (-)

» Class IX (14)

» Class X (16)

» Class XI (55)

» Class XII (53)

Economics Current (51)

International Affairs (20)

Polity and Governance (61)

Misc (77)

3.3 The Short Run and the Long Run

Short Run

•In the short run, at least one of the factor – labour or capital – cannot be varied, and therefore, remains fixed.

•In order to vary the output level, the firm can vary only the other factor.

•The factor that remains fixed is called the fixed factor.

•The other factor which the firm can vary is called the variable factor.

Example

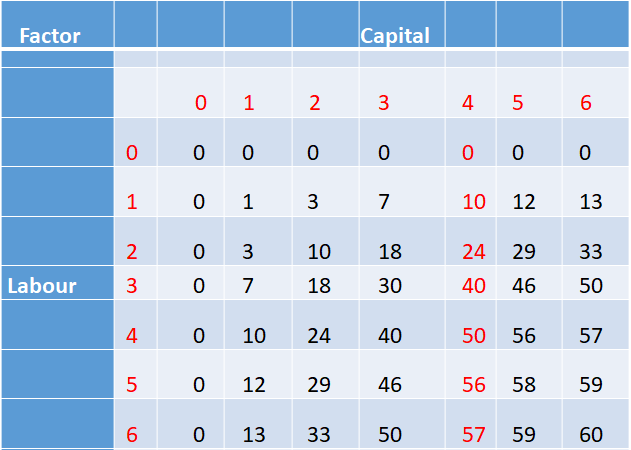

•In the Table, suppose, in the short run, capital remains fixed at 4 units.

•Then the corresponding column shows the different levels of output that the firm may produce using different quantities of labour in the short run.

Long Run

•In the long run, all factors of production can be varied.

•A firm in order to produce different levels of output in the long run may vary both the inputs simultaneously.

•So, in the long run, there is no fixed factor.

•For any particular production process, long run generally refers to a longer time period than the short run.

Short vs. Long Run

•For different production processes, the long run periods may be different.

•It is not advisable to define short run and long run in terms of period like days, months or years.

•We define a period as long run or short run simply by looking at whether all the inputs can be varied or not.

•The short run is unique to the firm, industry or economic variable being studied.

•In the long run, firms are able to adjust all costs, whereas, in the short run, firms are only able to influence prices through adjustments made to production levels.

•While a firm may be a monopoly in the short term, they may expect competition in the long run.

Key principle of short run and long run

•In the short run, firms face both variable and fixed costs, which means that output, wages and prices do not have full freedom to reach a new equilibrium.

•Equilibrium refers to a point in which opposing forces are balanced.

•We can thus usually change production as we don’t have control over other variables.

How a Long Run Works

•A long run is a time period during which a manufacturer or producer is flexible in its production decisions.

•Businesses can either expand or reduce production capacity or enter or exit an industry based on expected profits.

•Firms examining a long run understand that they cannot alter levels of production in order to reach an equilibrium between supply and demand.

An Example of a Long Run

•A business with a one-year lease will have its long run defined as any period longer than a year since it’s not bound by the lease agreement after that year.

•In the long run, the amount of labour, size of the factory, and production processes can be altered if need be to suit the needs of the business or lease issuer.

•Over the long run, a firm will search for the production technology that allows it to produce the desired level of output at the lowest cost else it may lose market share to competitors.

| Related Articles |

| Recent Articles |